Summary: Our Picks for the Best Home Insurance Companies

How Homeowners Can Find the Best Home Insurance

The best home insurance isn’t the same for everyone. Work with an insurance agent who can explain what home insurance covers and guide you in selecting the right coverage based on your property, family and situation. Knowing how home insurance works can help you identify the best home insurance providers for your specific circumstances.

Let’s look at a few common situations.

How to Compare the Best Home Insurance Companies

We suggest taking these steps to find the best home insurance.

- Determine how much coverage you need: Review each basic coverage type and adjust the limits to fit your specific needs. Make sure you have enough dwelling coverage to properly cover your home if it’s destroyed.

- Buy more coverage if you need it: You may find that you need additional coverage, such as higher liability limits and extended replacement or guaranteed replacement coverage. You can also buy umbrella insurance from top rated home insurance carriers, if your assets are beyond the policy’s liability limits.

- Fill in gaps: Your house insurance doesn’t cover all types of damage, but you can buy supplemental coverage like insurance for floods, earthquakes, water and sump overflow.

- Compare home insurance quotes: It’s smart to compare home insurance quotes from multiple insurance companies. Insurers’ rates can vary considerably for the same coverage, so it’s good to compare quotes from at least three reputable home insurance providers.

- Maximize home insurance discounts: Most reliable home insurance providers offer home insurance discounts that can reduce your policy costs. Bundling auto and home insurance often gets the best discounts, but you can also save by installing a security, fire safety or water leak-detection devices, going paperless, being a new customer, staying with a company for many years, renovating your home or multiple other ways. Talk to the insurance company about its discounts when getting quotes.

Tips for Finding the Best Home Insurance

Les Masterson

Insurance Editor

Ashlee Valentine

Insurance Editor

Michelle Megna

Insurance Lead Editor

Get the Right Dwelling Coverage Amount

Any reputable home insurance carrier or agent should be able to provide an estimate of how much it would cost to rebuild your house. This should be your dwelling coverage amount. One common mistake I’ve seen is that people confuse this amount with the real estate market value, but it’s not the same. And don’t include land value.

Insurance Editor

Ask About a Bundling Discount

One of the best insurance discounts is for bundling home and auto policies. We found that State Farm beats competitors with an average 23% multi-policy discount.

Insurance Editor

Get Multiple Quotes So You Know What’s a Good Deal

When shopping for home insurance, I recommend making sure you get quotes for the same coverage from at least three insurers. That will allow you to accurately determine who offers the best budget-friendly residential home insurance rates.

Insurance Lead Editor

Find the Best Home Insurance Companies in Your State

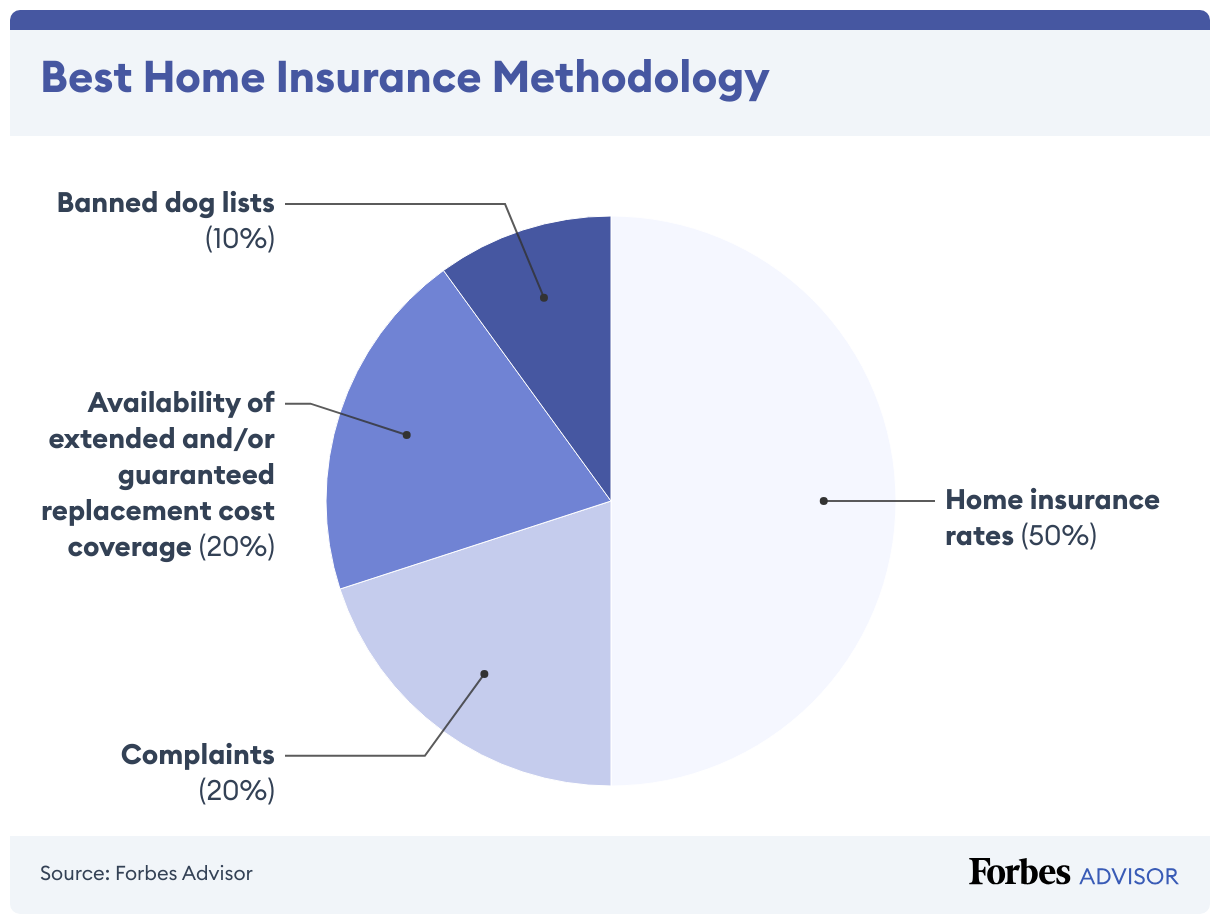

Methodology

To identify the best home insurance companies, we analyzed costs around the country, policy information and complaints against insurers. We scored companies based on these factors:

Home insurance rates (40% of score): We analyzed average rates for each insurance company for homes with dwelling coverage of $200,000, $350,000, $500,000 and $750,000 with 50% personal property coverage, 10% loss of use coverage, a $500 deductible, $1,000 guest medical coverage and $100,000 liability coverage for a 40-year-old woman with good credit.

Source: Quadrant Information Services.

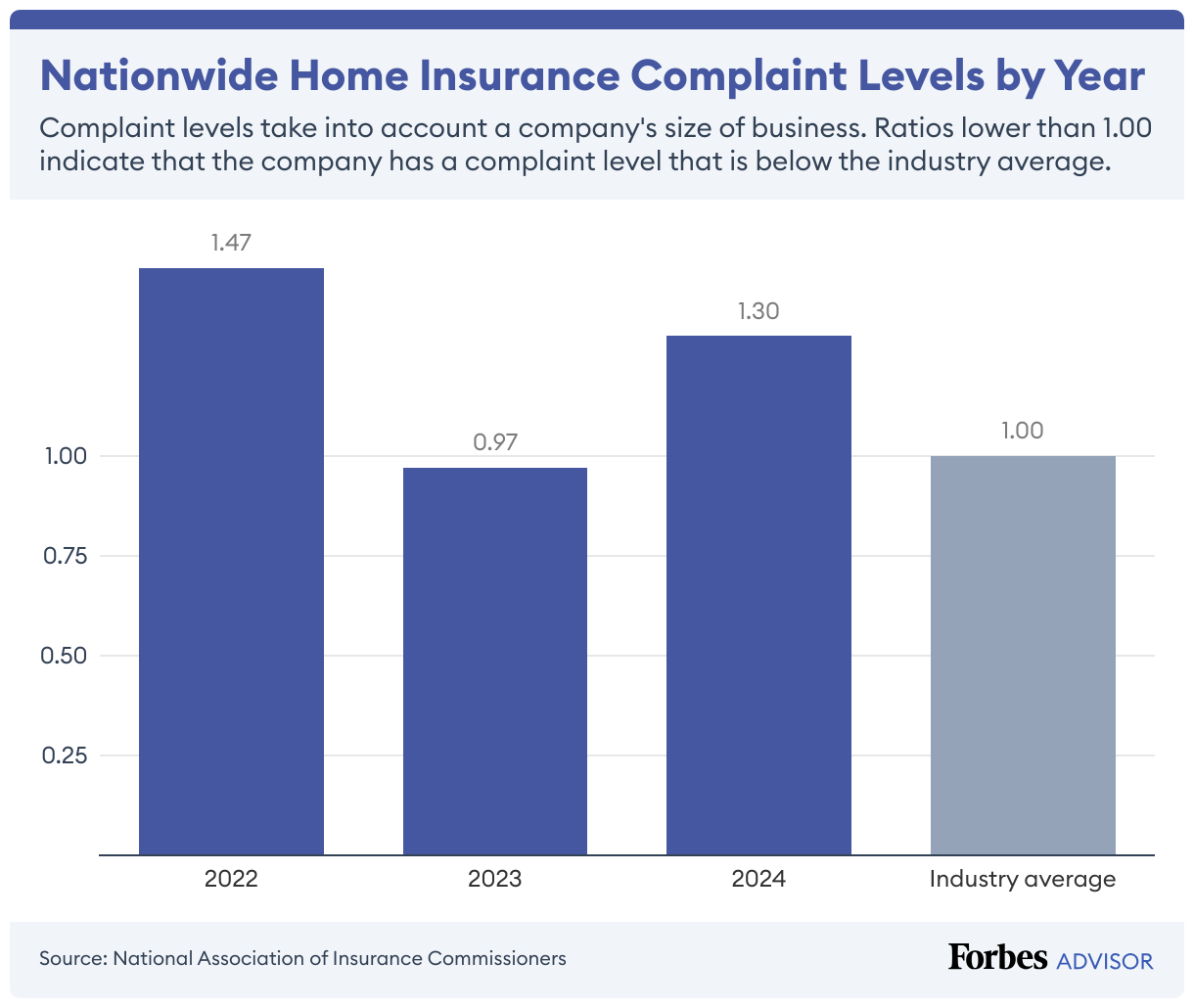

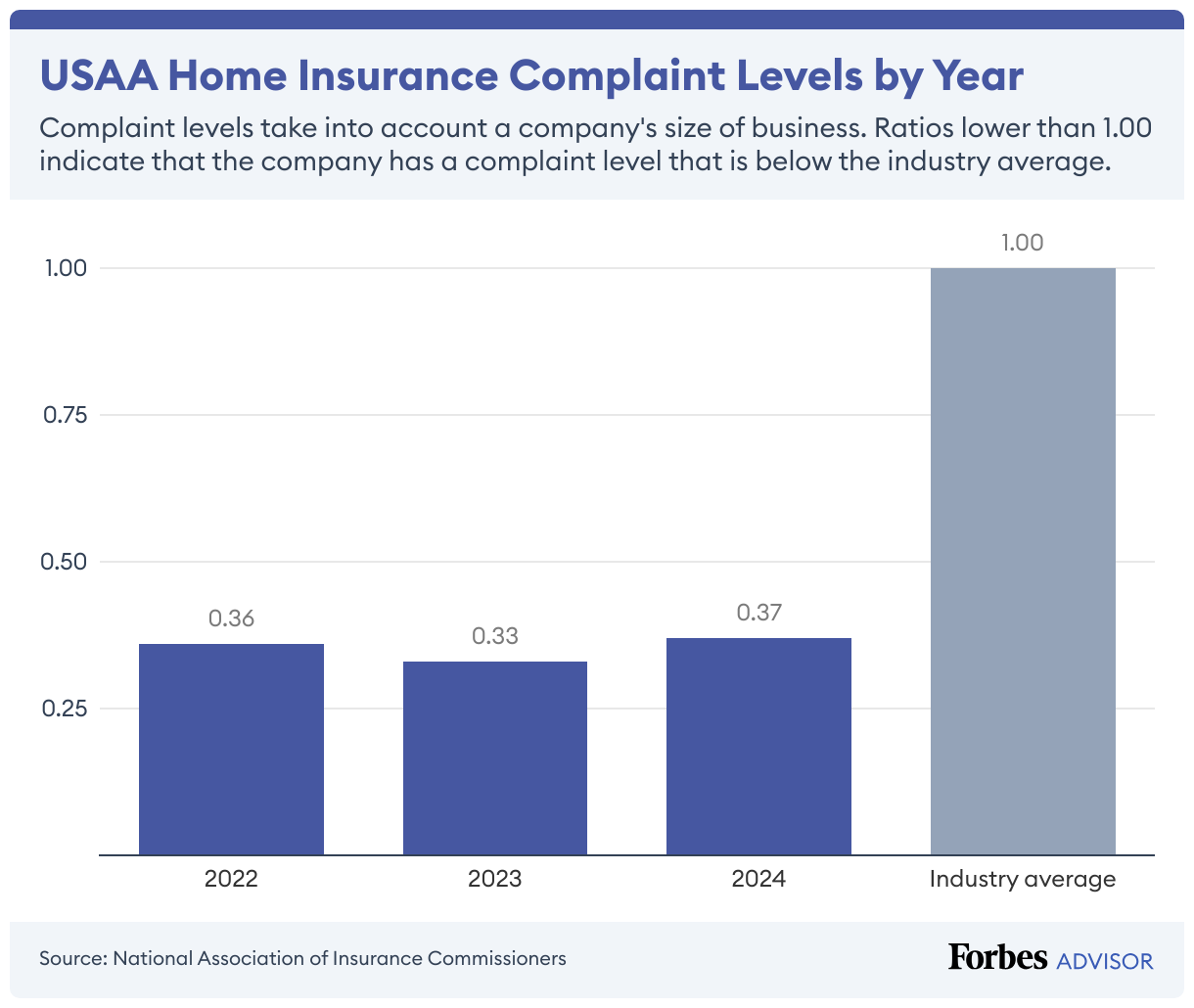

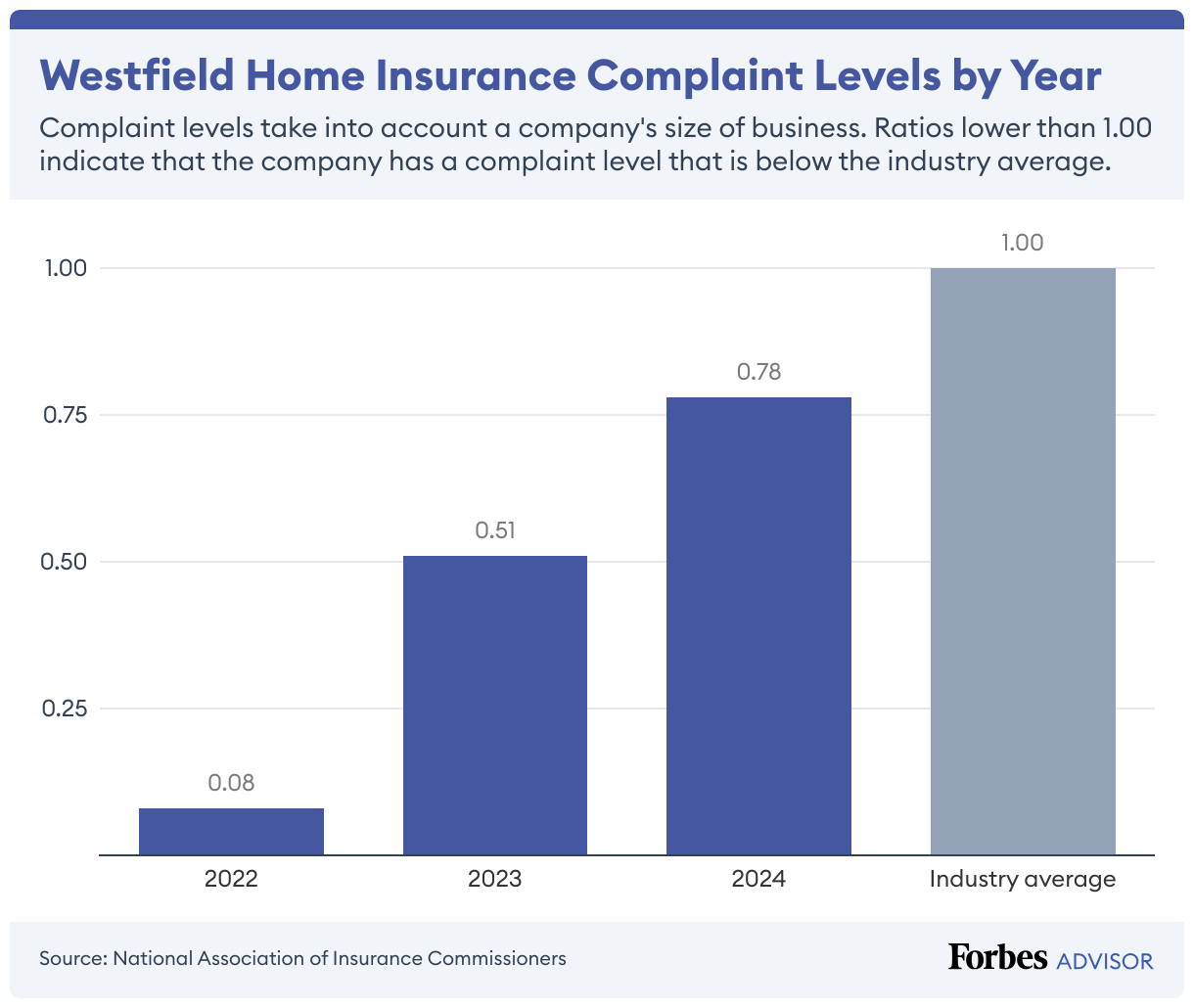

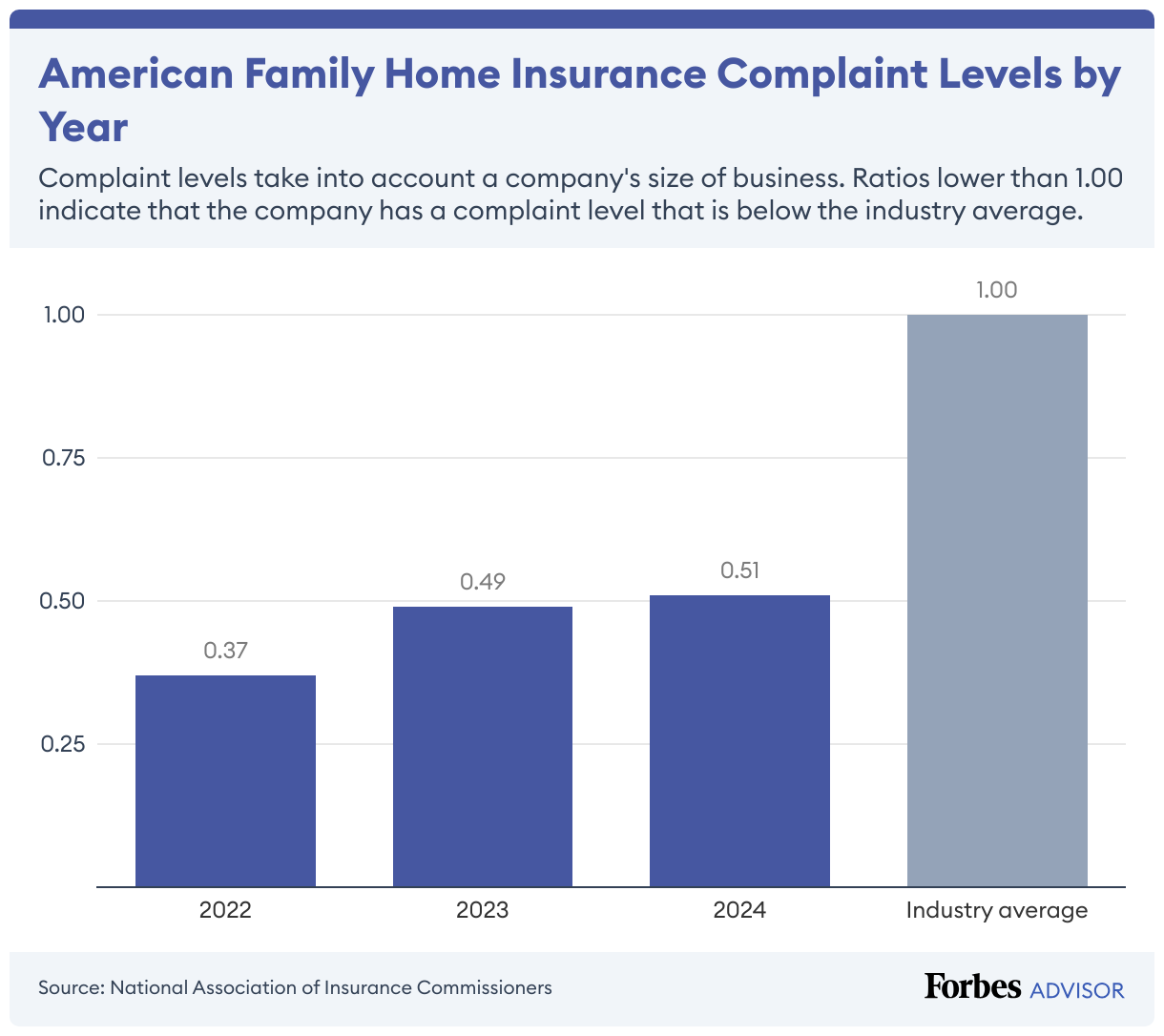

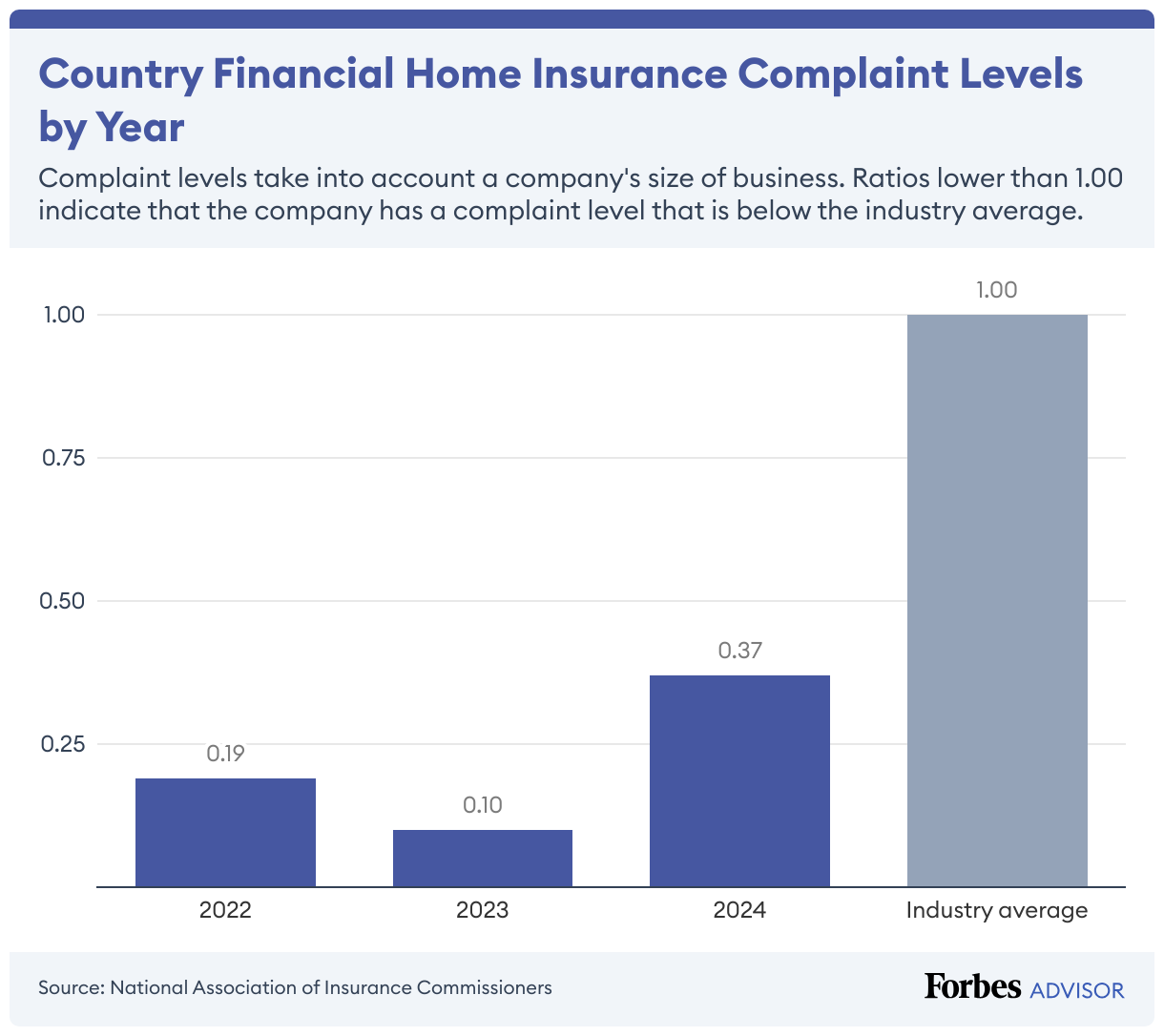

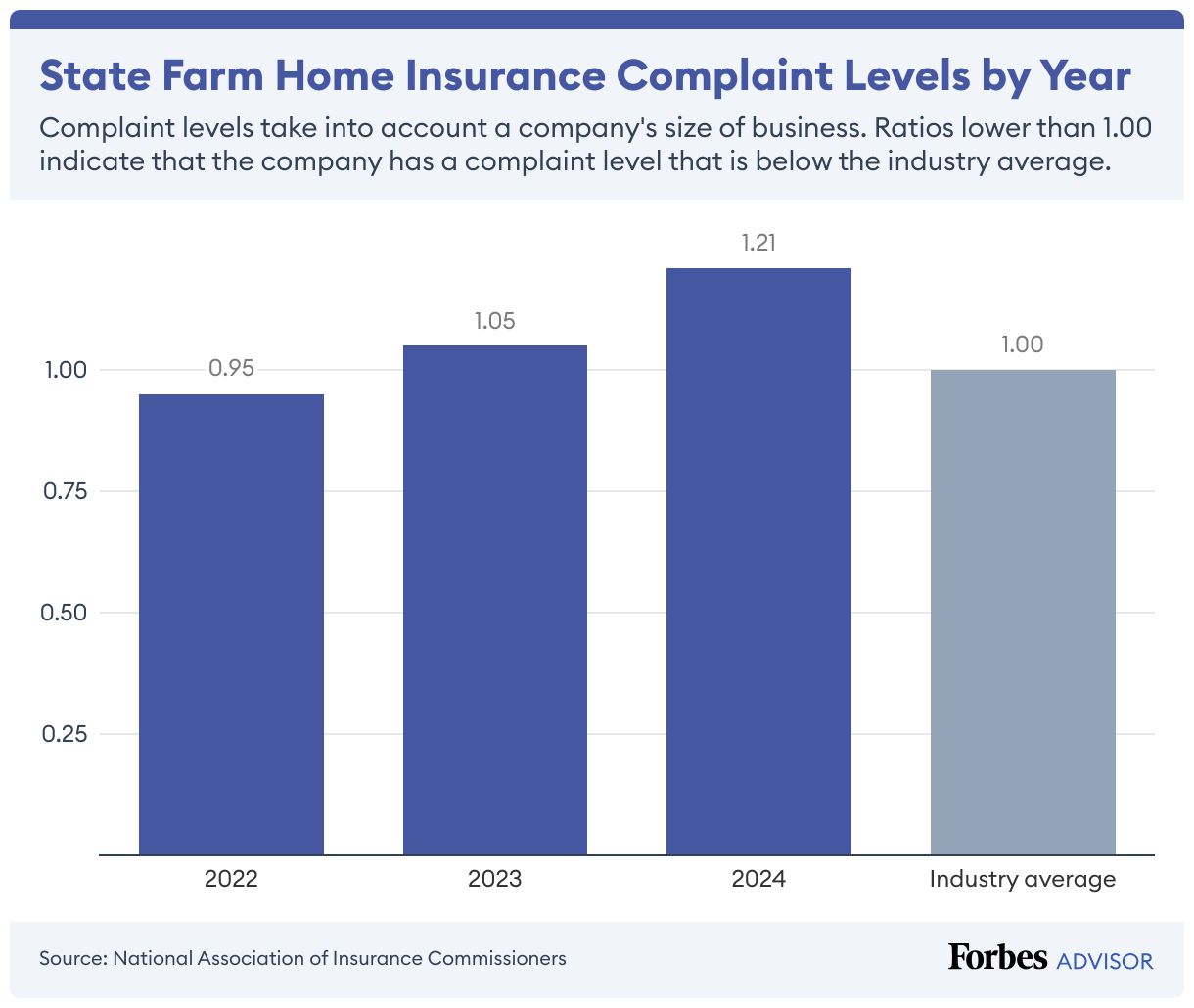

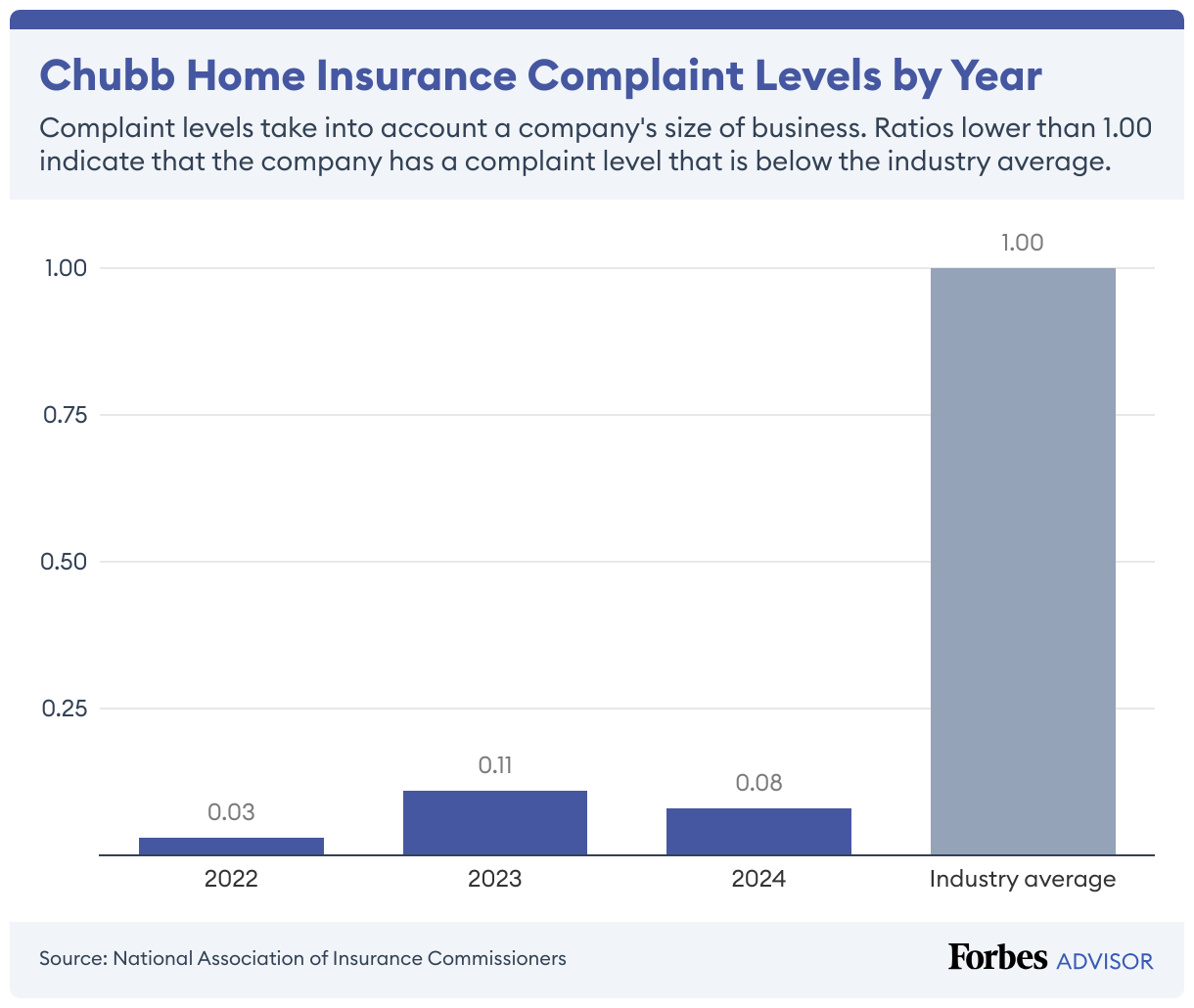

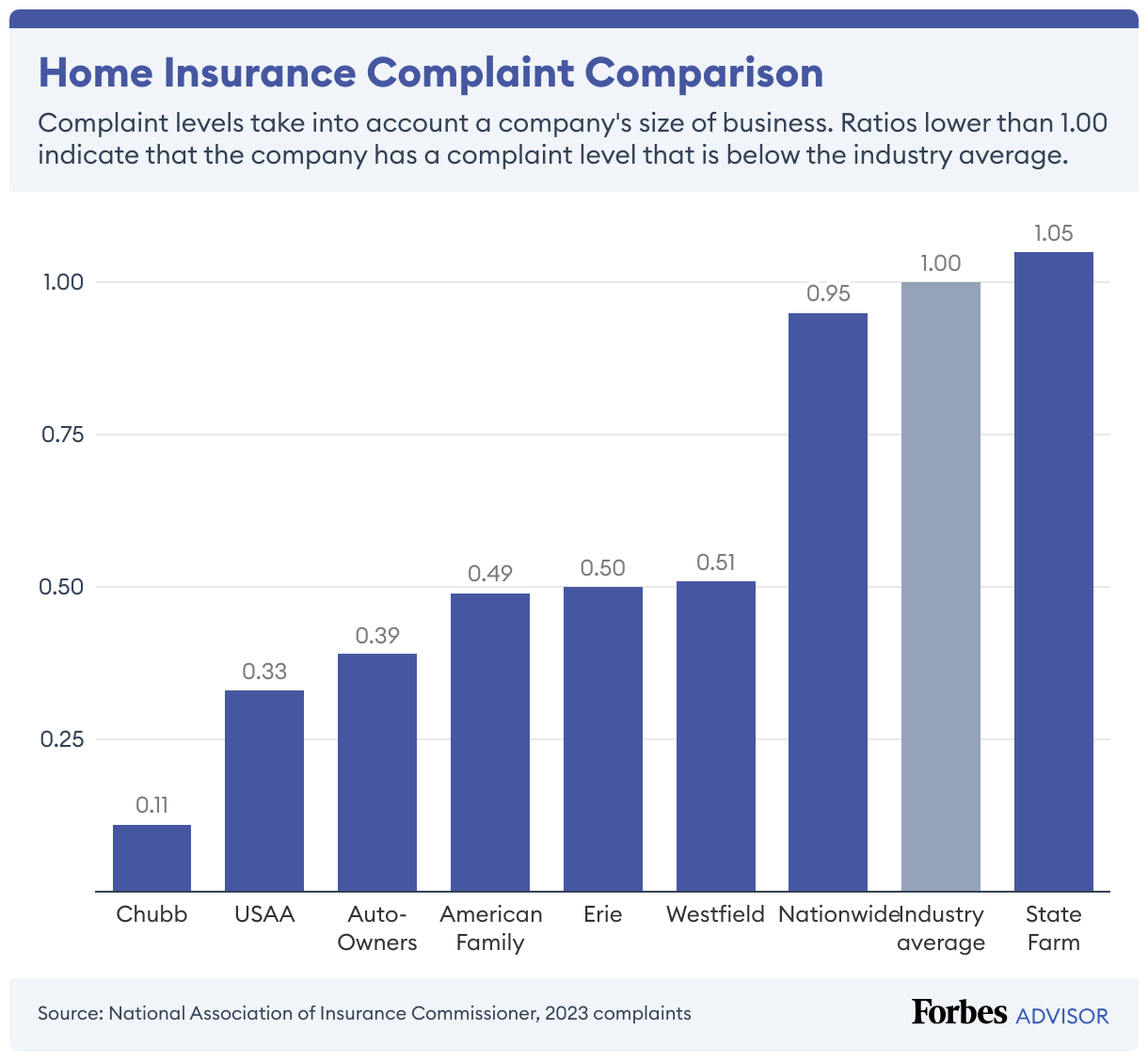

Complaints (20% of score): We used complaint data from state insurance departments across the country. Most home insurance complaints center on claims, including delays, unsatisfactory settlements and denials.

Source: National Association of Insurance Commissioners.

Availability of extended and/or guaranteed replacement cost coverage (20% of score): Extra dwelling coverage is valuable in the event of large disasters, when construction materials and labor costs tend to spike. We gave points to companies that offer either extended or guaranteed replacement cost coverage.

Source: Forbes Advisor research.

Digital experience (10% of score): We analyzed the quality of each company’s mobile app and website. We evaluated home insurers on:

- If there’s a mobile app.

- If you can submit claims online.

- If you can pay online.

- If there’s a useful website search function.

- If there’s a live chat that provides helpful information.

- If the company has a Facebook account that is updated regularly.

- If you can get a quote online.

Source: Forbes Advisor research.

Banned dog lists (10% of score): Banned dog breed lists can make homeowners ineligible for coverage. (A company’s banned dog list might not be applicable in all states.) While any homeowners insurance company could potentially ban any dog with a biting history, not all put a ban on specific breeds.

Source: Forbes Advisor research.

Read more: How Forbes Advisor rates home insurance companies

Looking for Homeowners Insurance?

Best Homeowners Insurance Frequently Asked Questions (FAQs)

What Is homeowners insurance?

Homeowners insurance is a contract between you and an insurance company that specifies how you’re compensated if your home and belongings are damaged due to unexpected events. It also outlines how you’re paid if you or your household members are liable for others’ injuries and property damage.

Who has the cheapest home insurance?

The cheapest home insurance companies are Progressive, Westfield, State Farm and USAA, based on our analysis.

Those are good starting points, but the most cost-effective home insurance carrier for you will vary depending on your location and the type of house you’re insuring. Shop around for a few home insurance quotes. And if you’re also getting car insurance quotes, ask about a discount for bundling auto and home insurance with the same company.

How do I file a homeowners insurance claim?

Contact the home insurance company or your insurance agent to file a home insurance claim over the phone, through the company’s website, chat, email or app, depending on the company. You want to document the loss by providing information about the cause, when it happened and a list of what was lost.

If your home was damaged, you should try to prevent more damage, such as boarding up a broken window. We wouldn’t suggest fixing the problem before contacting your insurance company. The insurer may want to send an adjuster to observe the damage. You should also keep damaged items so the insurer can document. Once the insurance company is done with its investigation, the insurer will offer a claims payout.

Is flood insurance included with my homeowners policy?

No, flood insurance isn’t typically covered as part of a home insurance policy. You instead need to buy a separate flood insurance policy.

You can purchase a National Flood Insurance Program policy from the Federal Emergency Management Agency (FEMA) or from a private insurance company.

How are homeowners insurance claims paid?

A claims adjuster will estimate the amount it will cost to fix your house and repair or replace damaged items. You’ll get an insurance check for that amount, minus your deductible and only up to your policy’s limits.

One of the best ways you can speed up your claims process and maximize your payment is by creating a home inventory. A good home inventory includes all of your personal belongings, including estimated values. You can create a simple list on paper, take pictures and video, or use a home inventory app.