You might be using an unsupported or outdated browser. To get the best possible experience please use the latest version of Chrome, Firefox, Safari, or Microsoft Edge to view this website.

We independently select all products and services. If you click through links we provide, we may earn a commission.

Learn More.

Taylor Medine is a staff writer at Forbes Advisor who demystifies complex money topics to help everyday people make more informed financial decisions. Over her nearly a decade of experience, Taylor's work has been published on Bankrate, Experian, Cre...

Taylor Medine is a staff writer at Forbes Advisor who demystifies complex money topics to help everyday people make more informed financial decisions. Over her nearly a decade of experience, Taylor's work has been published on Bankrate, Experian, Cre...

Taylor Medine is a staff writer at Forbes Advisor who demystifies complex money topics to help everyday people make more informed financial decisions. Over her nearly a decade of experience, Taylor's work has been published on Bankrate, Experian, Cre...

Taylor Medine is a staff writer at Forbes Advisor who demystifies complex money topics to help everyday people make more informed financial decisions. Over her nearly a decade of experience, Taylor's work has been published on Bankrate, Experian, Cre...

Mike Cetera is the editor in chief for Forbes Marketplace U.S. Mike has written and edited articles about mortgages, savings accounts, CD rates and credit cards for more than a decade. Prior to joining Marketplace, his work appeared on Bankrate, The...

Mike Cetera is the editor in chief for Forbes Marketplace U.S. Mike has written and edited articles about mortgages, savings accounts, CD rates and credit cards for more than a decade. Prior to joining Marketplace, his work appeared on Bankrate, The...

Mike Cetera is the editor in chief for Forbes Marketplace U.S. Mike has written and edited articles about mortgages, savings accounts, CD rates and credit cards for more than a decade. Prior to joining Marketplace, his work appeared on Bankrate, The...

Mike Cetera is the editor in chief for Forbes Marketplace U.S. Mike has written and edited articles about mortgages, savings accounts, CD rates and credit cards for more than a decade. Prior to joining Marketplace, his work appeared on Bankrate, The...

Editorial Note: We earn a commission from partner links on Forbes Advisor. Commissions do not affect our editors' opinions or evaluations.

When you have bad credit, payday loans aren’t your only avenue for borrowing. To help you find the best bad-credit loan, our data research team reviewed loans from popular lenders to identify options you may qualify for with a credit score below 580.

We scored and ranked lenders across categories, such as loan affordability, since that’s a top concern when shopping for a loan with bad credit. Each lender on our list offers installment loans with repayment terms that last several months rather than just a few weeks, which is typical of high-fee payday loans. Continue reading for an overview of each top-ranking lender and learn best practices for finding an affordable loan.

Our editorial team has over 20 years of cumulative experience and relies on research and data-driven methodologies to provide unbiased ratings for emergency loans. We are not influenced by advertisers and provide honest and transparent product evaluations. You can read more about our editorial guidelines and the loans methodology below.

Our ratings take into account loan cost, loan details, eligibility and accessibility, customer experience and application process. All ratings are determined solely by our editorial team.

Upstart uses an underwriting approach that reviews 1,600 data points to evaluate borrower risk and set interest rates. For example, Upstart considers factors like your education level and area of study to determine loan approval, not just your credit score.

Why We Like It

We like that Upstart has an innovative application review process that can make loans available to borrowers with limited credit. Loan funding can also happen within a business day.

Why We Don’t Like It

We don’t like that the loan origination fee is up to 12%, which is high. Plus, only two loan terms are available—36 months and 60 months—so you have limited repayment schedules.

Who It’s Best For

Upstart loans are best for borrowers who want to take out a large loan but lack a positive credit history. If you shine in other areas, like having advanced education and stable employment, these factors could tip the approval scale in your favor.

Pros & Cons

Loans up to $50,000

No prepayment penalty

Low income requirement

High origination fees

Limited repayment terms

Co-borrowers and co-signers not permitted

Details

Eligibility

Minimum credit score. 300

Minimum annual income. $12,000

Co-borrowers/co-signers. Not permitted

Funding Speed

Funding can happen in as little as 24 hours.

*Upstart’s minimum credit score is 300, but prequalification through Credible starts at 620.

Best for Flexible Repayment Terms

Avant

4.1

Our ratings take into account loan cost, loan details, eligibility and accessibility, customer experience and application process. All ratings are determined solely by our editorial team.

Minimum Credit Score

550

APR range

9.95% to 35.99%

Loan amounts

Example: A $5,900 loan with an administration fee of 4.75% and an amount financed of $5,619.75, repayable in 36 monthly installments, with an APR of 29.95% would have monthly payments of $250.30. If approved, the actual loan terms that a customer qualifies for may vary based on credit determination, state law, and other factors. Minimum loan amounts vary by state.

Example: A $5,900 loan with an administration fee of 4.75% and an amount financed of $5,619.75, repayable in 36 monthly installments, with an APR of 29.95% would have monthly payments of $250.30. If approved, the actual loan terms that a customer qualifies for may vary based on credit determination, state law, and other factors. Minimum loan amounts vary by state.

$2,000 to $35,000

Editor’s Take

Avant’s mission is to provide borrowing opportunities for everyday people. While Avant doesn’t have physical locations, customer service has office hours throughout the week and weekend if you want to speak with a live person about loans.

Why We Like It

We like that Avant offers multiple loan term options ranging from two to five years, depending on your state.

Why We Don’t Like It

We don’t like the high loan administrative fee of up to 9.99% of your loan amount. However, if you pay off your loan in full before the maturity date, Avant may refund the portion of the fee over 5% on a prorated basis.

Who It’s Best For

Avant loans are best for borrowers who want the flexibility to choose between multiple repayment schedules since Avant may provide applicants with numerous loan offers.

Pros & Cons

No prepayment penalty fees

Refundable origination fee if the loan is repaid early

Accessible customer services hours

High origination fees

Co-signers and co-borrowers not permitted

Details

Eligibility:

Minimum credit score. 550

Minimum annual income. $14,400

Co-borrowers/co-signers. Not permitted

Funding Speed

Funding can happen the next business day.

Best for Same-Day Funding

OppLoans

3.5

Our ratings take into account loan cost, loan details, eligibility and accessibility, customer experience and application process. All ratings are determined solely by our editorial team.

OppLoans provides short-term loans to borrowers with poor or limited credit by assessing banking history and overall financial stability during the application review process. Only a soft inquiry is performed during the application, so applying won’t cause a negative credit hit.

Why We Like It

OppLoan charges no origination fee. In comparison, most other online lenders charge borrowers an origination or administrative fee. Same-day funding may also be available.

Why We Don’t Like It

The lack of origination fees doesn’t mean loans are affordable. Interest rates on loans from OppLoans can still be very high. Therefore, it’s important to consider OppLoans as a last resort only after comparing it against other loans and financing options.

Who It’s Best For

OppLoans are best for borrowers who need to borrow a small sum for an emergency and cannot qualify for loans with more competitive rates.

Pros & Cons

No prepayment penalty fees

No credit score minimum

No origination fee

High interest rates

Co-signers and co-borrowers not permitted

Details

Eligibility

Minimum credit score. No minimum

Minimum income. Not disclosed.

Co-borrowers/co-signers. Not permitted

Funding Speed

If verification is complete and you get a final approval before 12 p.m. CT., you can have funding as soon as the same day.

Most Popular is calculated from the number of times each affiliate product was selected by Forbes users over a six month time period.

How To Compare Loans for Bad Credit

When you have bad credit, shopping around is the best way to find the most affordable loan.

Bad credit loans typically have higher interest rates and fees than other personal loans. That’s because borrowers with bad credit are more likely to miss payments, and lenders tend to charge more to offset that financial risk. The tips below can help you compare loan options.

Evaluate qualification requirements. Many lenders share minimum credit and income conditions on their websites. Some lenders may even offer no-credit-check loans. Review eligibility conditions to narrow down loans that best fit your credit profile.

Review annual percentage rates (APRs). An APR is a percentage that expresses the annualized cost of borrowing, including fees. Reviewing APRs from multiple lenders can help you effectively compare loan costs head-to-head.

Check repayment terms. Depending on the lender, loan terms on bad credit loans range from as short as a few weeks to a year or more. Consider your reason for borrowing to determine which loan term would best suit your financial needs.

Understand fees and penalties. In addition to ongoing interest, lenders may charge upfront loan processing fees or penalty fees for paying late. Compare extra fine print costs to determine where you’ll find the most savings.

Consider processing and funding speeds. Lenders vary in how long it takes to apply, get approved and receive loan funds. If you need cash quickly, consider looking for loans with fast approvals and same-day or next-day funding.

See if co-signers are accepted. Not all lenders accept co-signers or co-borrowers, but if they do, adding one to your loan could help you get a better interest rate.

Prequalify when you can. Many lenders have online prequalification forms you can use to check rates without a hard credit check. Prequalify with multiple lenders to measure costs and test the likelihood of approval.

What Is a Personal Loan for Bad Credit?

Bad-credit loans are loans you may qualify for with a credit score close to or below 580.

Installment loans and payday loans (sometimes called cash advances) are types of loans that can fall into the bad-credit loan category. Installment loans offer you a lump sum often deposited into your bank account, and payments are due monthly until the loan is paid off.

On the other hand, payday loans are typically due in full by your next paycheck unless you request to roll over the loan to a new term for an additional fee.

Here are the important features of a bad credit loan:

Interest Rates and Fees

A major pitfall of bad credit loans is high interest rates. Interest rates are what lenders charge you to borrow money. Since the annual percentage rate (APR) is a rate percentage that includes extra fees, it gives you a more complete picture of how much a loan costs. Some bad credit loans can have high rates of 100% to 400% APR.

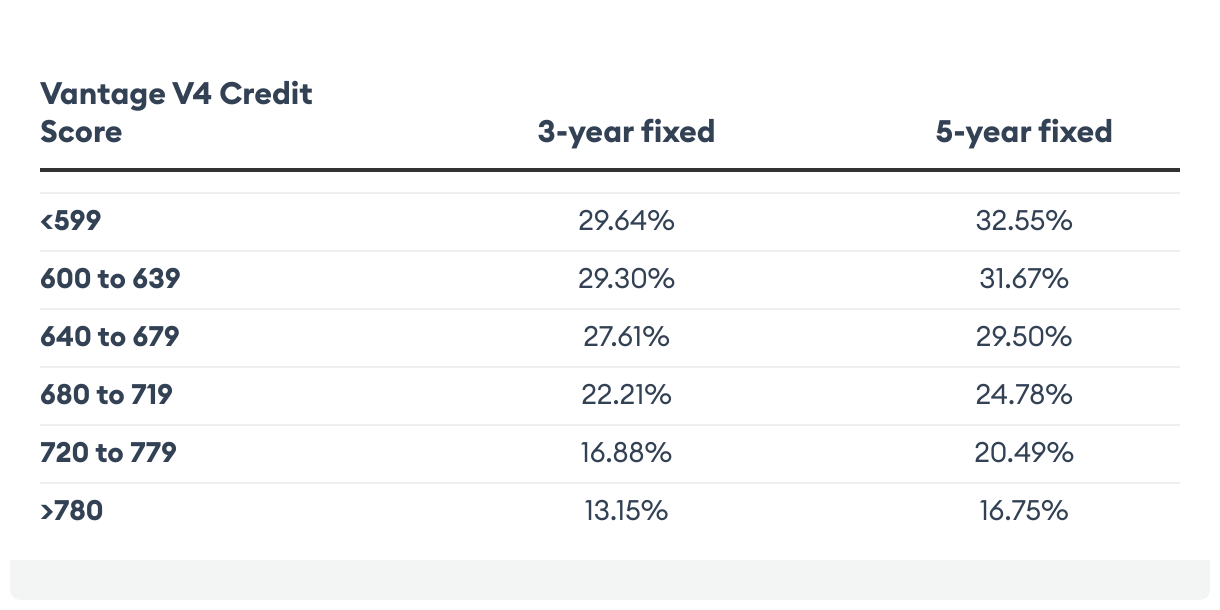

Average Interest Rates by Credit Score

In comparison, below are average loan rates for borrowers who have fair credit or better based on data from Credible. Keep in mind that rates may vary from one borrower to the next.

Amounts

Generally, installment loan amounts start at $500 to $1,000. However, payday loans and cash advances may limit loan amounts to less than $500.

Ultimately, how much you qualify for will depend on application factors, such as your income. Some lenders that offer installment loans provide loans of up to $50,000; however, the higher amounts are usually for borrowers with stronger credit profiles.

Terms

Bad-credit loans may have shorter terms. When shopping around, you might run into lenders offering terms up to 84 months, but the longest terms are usually unavailable to borrowers with bad credit.

How To Get a Loan With Bad Credit

When applying for a bad credit loan, lenders may heavily consider other data points, such as your income and employment. Taking the steps below could help you get a loan.

Maintain a steady job. Having a steady cash flow can show lenders you have the financial means to repay debt despite negative credit history.

Pledge collateral. If you have some savings stashed away, use it to your advantage. Some lenders accept cash in a savings account or certificate of deposit (CD) as collateral to back a loan, which can increase your approval odds and lower your rate.

Pay down debt. Paying off other existing debt obligations before borrowing can make you look like a less risky loan applicant.

Clean up your credit. Cleaning up your credit report could boost your score and increase your chances of approval. Each credit bureau has instructions on its website on how to dispute credit report records.

Shop around. Credit requirements vary; shopping around is the best way to find lenders willing to loan you money.

Guaranteed Loans

Guaranteed loans are a type of bad credit loan in which approval is nearly guaranteed without a credit check, as long as you meet the application requirements.

Like other loans for bad credit, guaranteed loans tend to have higher interest rates and fees, so it’s essential to understand the total costs before committing to the loan.

How To Get a Personal Loan With Bad Credit

If you need a loan with bad credit, the steps below can help you get approved.

Get together proof of income. The higher and more consistent your income, the greater your chances of approval. Lenders may accept multiple sources of income on the application, such as alimony or child support.

Look for a co-signer. If you feel comfortable, ask someone you know to cosign your loan. This gives you a shot at securing a better rate, which can result in interest savings.

Prequalify if you can. Many lenders allow you to check loan interest rates by prequalifying online with just a soft credit inquiry.

Weigh multiple options. Since credit requirements, terms and rates vary, contact several lenders to review options before accepting the first offer.

Alternatives to Bad Credit Loans

Bad-credit loans are just one way to borrow money when your credit score falls into the “poor” range, which is 579 or below on the FICO Score scale. Below are alternatives you could consider.

Credit union loans. Federal credit unions may offer low-interest payday alternative loans (PALs) of $200 to $1,000 to members who need quick cash. Consider scoping out credit unions and membership requirements to see if you qualify.

Credit cards. Using a credit card to make purchases or request a cash advance is one way to bridge a financial gap. However, interest rates and advance fees can be high. Avoid revolving a high balance when using a card, as this can cause debt to grow out of control.

Home equity financing. Home equity loans or credit lines are secured financing backed by your home. If you qualify, home equity products may offer better rates than unsecured personal loans, but you have to consider the loan closing fees in your cost analysis.

Loan apps. Certain apps like Earnin and Dave offer small loans without credit checks and no fees, making them potentially cheaper than other installment loans for bad credit.

Payroll advances. Some employers offer employee loans or advances from future paychecks to help workers meet financial needs. Terms, conditions and fees vary, so you’ll have to contact your employer to see if this option is available.

Peer loans. Asking someone you know for a small sum of cash can be less expensive than taking out a bad credit loan, and you don’t have to go through an application or credit check process. But since unpaid debt to family and friends can cause conflict, you should take repayment of a peer loan as seriously as any other loan.

Methodology

We reviewed 35 popular lenders based on 19 data points in the categories of loan details, loan costs, eligibility and accessibility, customer experience and the application process. We chose lenders that have a minimum credit score requirement of 580 or lower and ranked them based on the weighting assigned to each category:

Loan cost. 32%

Eligibility and accessibility. 21%

Loan details. 20%

Customer experience. 16%

Application process. 11%

Within each category, we also considered several characteristics, including loan amounts, repayment terms, APR ranges and applicable fees. We also looked at whether each lender accepts co-signers or joint applications and the geographic availability of the lender. Finally, we evaluated each provider’s customer support tools, borrower perks and features that simplify the borrowing process—like prequalification and mobile apps.

Where appropriate, we awarded partial points depending on how well a lender met each criterion.

What is the easiest type of loan to get with bad credit?

The easiest types of loans to get with bad credit are typically no-credit-check loans, including payday, title and pawnshop loans. However, these debts come with excessive fees, and we recommend avoiding them. Instead, lean into personal loans for bad credit, like those on this list. Some lenders make loans available to applicants with credit scores as low as 550.

Can you get a personal loan with a credit score of 550?

There aren’t many lenders that accept applications from borrowers with credit scores of 550. However, there are lenders who allow for a co-signer—someone who agrees to repay the loan if the primary borrower cannot—which can help you qualify for a loan with a score of 550. If you know you have damaged credit, look to improve your credit before applying for a personal loan.

Can you get a loan with no credit check?

While most loans require a credit check, there are some loans that don’t. Instead, lenders qualify applications based on the applicant’s ability to repay the loan. Lenders will likely also require collateral—a personal asset used to secure a loan and one the lender can repossess if the repayment terms are not met. You can get no-credit-check loans through payday loan stores, auto title lenders, online lenders and pawn shops.

How much money can you borrow with bad credit?

A lender typically determines your loan limit based on your creditworthiness and income. The largest limits are reserved for high-qualified borrowers. If you have bad credit, you can expect to receive near the minimum loan limit your lender offers. If you need to borrow more money, consider improving your credit score prior to applying.

Is there risk in bad credit loans?

Whenever you get a bad credit personal loan, you take on some level of risk. While most personal loans are unsecured, meaning you don’t need to provide collateral to secure the loan (and therefore avoid losing a personal asset if you fail to meet the repayment terms), you still risk damaging your credit score if you don’t keep up with your monthly payments.

How do you fix bad credit to get a better loan?

If you know you have bad credit and are preparing to apply for a loan, take time to improve your credit score. Some common ways to do that include paying off your existing debts, reducing your overall credit usage, disputing any errors on your credit report and reducing the number of new credit applications made in a short period of time.

Information provided on Forbes Advisor is for educational purposes only. Your financial situation is unique and the products and services we review may not be right for your circumstances. We do not offer financial advice, advisory or brokerage services, nor do we recommend or advise individuals or to buy or sell particular stocks or securities. Performance information may have changed since the time of publication. Past performance is not indicative of future results.

Forbes Advisor adheres to strict editorial integrity standards. To the best of our knowledge, all content is accurate as of the date posted, though offers contained herein may no longer be available. The opinions expressed are the author’s alone and have not been provided, approved, or otherwise endorsed by our partners.

Taylor Medine is a staff writer at Forbes Advisor who demystifies complex money topics to help everyday people make more informed financial decisions. Over her nearly a decade of experience, Taylor's work has been published on Bankrate, Experian, Credit Karma, MarketWatch, The Balance and more.

Mike Cetera is the editor in chief for Forbes Marketplace U.S. Mike has written and edited articles about mortgages, savings accounts, CD rates and credit cards for more than a decade. Prior to joining Marketplace, his work appeared on Bankrate, The Points Guy and Fit Small Business. Mike earned a master’s degree in public affairs reporting from the University of Illinois and has been a journalist for more than two decades. He also has offered his expertise in numerous TV, radio and print interviews.

Was this article helpful?

Send feedback to the editorial team

Thank You for your feedback!

Something went wrong. Please try again later.

The Forbes Advisor editorial team is independent and objective. To help support our reporting work, and to continue our ability to provide this content for free to our readers, we receive compensation from the companies that advertise on the Forbes Advisor site. This compensation comes from two main sources. First, we provide paid placements to advertisers to present their offers. The compensation we receive for those placements affects how and where advertisers' offers appear on the site. This site does not include all companies or products available within the market. Second, we also include links to advertisers' offers in some of our articles; these “affiliate links” may generate income for our site when you click on them. The compensation we receive from advertisers does not influence the recommendations or advice our editorial team provides in our articles or otherwise impact any of the editorial content on Forbes Advisor. While we work hard to provide accurate and up to date information that we think you will find relevant, Forbes Advisor does not and cannot guarantee that any information provided is complete and makes no representations or warranties in connection thereto, nor to the accuracy or applicability thereof. Here is a list of our partners who offer products that we have affiliate links for.